ASRS aligned

Site-specific

Quantitative outputs

Board defensible

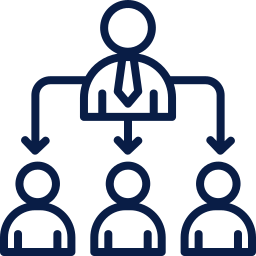

Climate hazards identified

Heat, rainfall, cyclones, bushfire and other relevant hazards assessed by location and scenario.

Operational impact quantified

Hazards translated into lost productive days and disruption metrics.

Financial exposure calculated

Lost production converted into revenue, margin, or cost impact.

Decision-ready outputs delivered

Board-ready summaries aligned to ASRS requirements.

Mining and resources

Energy and infrastructure

Industrial and logistics operations

Agriculture and land-based assets

Government planning and funding assessment